By Matthew Dilks, Bridging and Commercial Specialist, Clever Lending

In the property investment and development world, gross development value (GDV) is an important metric used to determine what a project may be worth on the open market once all the planned works have been completed.

Significance of GDV

Gross development value is a significant calculation as it is the foundation on which all other aspects of a build are determined. This includes the cost of acquiring the development site, the cost of construction and other associated works, the profit margin of the developer or investor and the likelihood of a successful and profitable financial outcome.

Stephen Henman, Managing Director at Method Valuation UK, said:

“The way in which GDV is calculated is extremely complex and can prove to be a minefield for many brokers, particularly those unfamiliar with working in this area of the specialist lending market.”

“At Method we see at close quarters the impact of the complex nature of GDV calculations. This can occasionally cause friction during the valuation process and is exacerbated by current market conditions,” he says.

“It’s important that brokers and lenders are fully aware of the contributing factors to the GDV calculation, particularly the impact of the developers anticipated profit margin on the GDV.”

Lender-Specific Criteria

Understanding the way in which lenders calculate GDV is crucial to securing funding in any development finance project because it can vary hugely between projects and also differs vastly from the standard loan-to-value (LTV) ratios used in residential mortgage loans.

Different lenders also use different methods to determine affordability, with the most common being the GDV plus costs. This can typically be between 50% to 70% GDV plus up to 100% of the construction and development costs, but will depend on the size of the deposit, the experience of the developer, the feasibility of the project and the planned exit strategy.

Each lender also has its own lending criteria as well as a minimum and maximum on borrowing amounts, which can range between £50,000 and £50 million. Proof of a solid exit strategy will also be critical as your ability to sell or remortgage the development will also determine the GDV value.

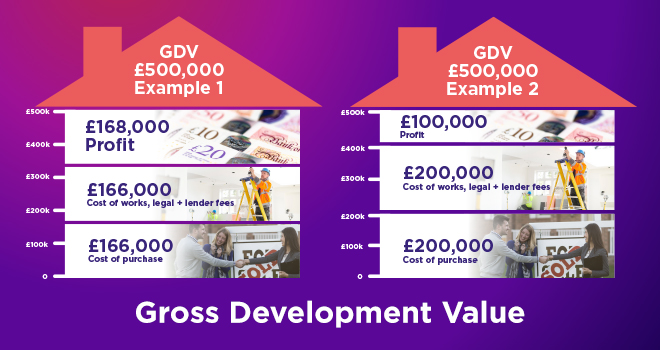

As a general rule, lenders like to see an expected 20% minimum profit built into any development plan, with the GDV calculation split into thirds across the purchase cost, the cost of works and projected profit. Examples of this can be seen in the figures below, with example 1 showing the three splits and example 2 showing a 20% profit.

Day One Valuation

Lenders also tend to work backwards from the GDV calculation to work out the current valuation for day one of the lend and will deduct any expenses, development costs and contingency costs built into the calculations which can result in a lower valuation than what the client may expect.

Understanding this is crucial as it can sometimes be an issue on day one of lending as clients may find the current value to be quite a bit lower than what they expected. This is an important factor to take into consideration as it could impact the project and cause delays.

Seeking Expert Guidance

Calculating GDVs is an extremely complex process so brokers who are unsure of how a case should progress, should talk to a trusted development finance expert who can help them through the process. This will not only help to alleviate the pressure of placing the business, but also ensure they are providing their clients with an accurate GDV calculation on any planned development finance project.