Bridging loan transactions bounce back to pre-pandemic levels as stock shortages put pressure on buyers to move quickly

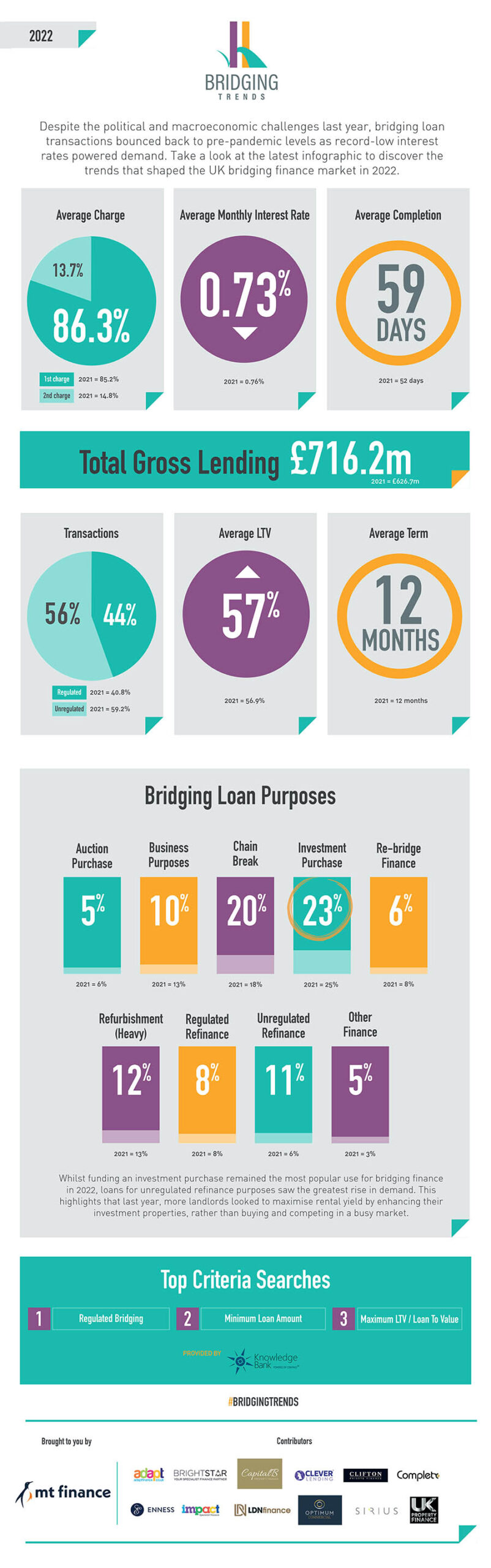

Annual demand for bridging loans increased to the highest figure since 2019, as £716.2 million of bridging loans were transacted by contributors in 2022, according to the latest Bridging Trends data.

Key Points for 2022:

- Gross contributor lending up 14%

- Interest rates fell to lowest level recorded

- Completion times climb as industry feels pressure

- Regulated bridging demand increases

£716.2 million of bridging loans were transacted by Bridging Trends contributors in 2022. A 14% increase on the £626.7 million transacted in 2021 – the highest annual figure reported since 2019 (£732.7 million).

The bridging loan market withstood numerous challenges throughout 2022, including the conflict in Ukraine, soaring inflation, the subsequent cost-of-living crisis, and political uncertainty caused by September’s disastrous mini-Budget. Despite this, all four quarters in 2022 reported year-on-year growth in contributor lending (Q1 £156.8m, Q2 £178.4m and Q4 £166.3m) with transactions peaking in the third quarter at £214.7m – the highest level of loans transacted by contributors in a single quarter since Bridging Trends launched in 2015.

The average annual interest rate fell to the lowest level in 2022 to 0.73%, down from 0.76% in 2021 and 0.79% in 2020.

Strong competition between lenders amidst the Bank of England rate hikes pushed down rates in the first three quarters of the year. However, Q4 2022 saw a sharp spike in pricing following September’s mini-Budget, with the average monthly rate increasing to 0.79%, up from 0.73% in Q3.

The average loan-to-value in 2022 was static, at 57%, reflecting that despite market competition, a conservative and sensible approach to lending is being maintained.

Funding an investment purchase remained the most popular use for bridging finance in 2022, although demand decreased from 25% in 2021 to 23% in 2022. Meanwhile, loans for unregulated refinance purposes saw the greatest increase in demand, surging to 11% of total transactions in 2022 from 6% in 2021. This shows that property investors and landlords looked to maximise rental yield by enhancing their investment properties in 2022, rather than buy and compete in a busy market.

Continued shortage of housing stock meant there was serious competition and pressure on buyers this year. This resulted in an increasing number of homeowners turning to bridging finance with regulated transactions accounting for 44% of all bridging loans in 2022, up from 40.8% in 2021. The need for rapid transactions was further highlighted by the rise in bridging loans being used to prevent chain breaks, which rose from 18% in 2021 to 20% in 2022.

Second charge bridging loans accounted for 13.7% of contributor transactions in 2022, a drop from 14.8% in 2021 and a new record low for annual Bridging Trends data. This dip could be due to borrowers looking to move and purchase new properties than releasing equity in their current assets.

The average loan term in 2022 was once again 12 months, while the average completion time for a bridging loan crept up to 59 days. This increased from 52 days in 2021 and is an indicator of both the product’s increasing popularity and the pressure on industry professionals, particularly in the wake of September’s mini-Budget.

According to data supplied by Knowledge Bank, the top criteria search made by bridging finance brokers in 2022 was for ‘regulated bridging’ which further indicates the growing demand for regulated products. This was followed by ‘minimum loan amount’ and ‘maximum LTV’.

In 2021, the top criteria search made on the Knowledge Bank system was for ‘maximum LTV’.

Dale Jannels, managing director of Impact Specialist Finance comments:

“With the lack of housing stock unlikely to change in 2023, along with continued affordability challenges for borrowers due to increased interest rates, the use of regulated bridging to fund onward purchases before their current home is sold will remain a viable option. I do not expect to see a reduction in its use any time soon.

It is also interesting to see an increase in unregulated refinance and I expect to see this trend continue with landlords making HMO conversions, plus a realisation from more and more landlords that the EPC regulations aren’t going away. This will lead to more improvements will be made to improve energy efficiency in older properties especially.

Chris Whitney, head of specialist lending at Enness comments:

The 2021, 2022 comparison doesn’t really give us any surprising data. Both years had their challenges for different reasons in terms of the macro economy. However, the numbers seem to indicate that borrowers were very much in a ‘keep calm and carry on’ mentality. I think we saw lenders (in the main) take the same view and adapt to things like cost of funds increases swiftly. Still modest LTV’s overall, indicating responsible borrowing and lending.

The healthy increase in borrowing was nice to see and confirms what we already know, the bridging finance market has matured, here to stay, and a tool increasingly used by borrowers as a matter of course rather than just by exception.

2023 will, I am sure, also have its challenges but the mood in the market as we kick the year off seems hugely positive.

Sam O’Neill head of bridging at Clifton Private Finance comments:

It’s good to see faith in the bridging market back to pre-pandemic levels. Bridging loans plugged a large gap during Covid-19 for SDLT cuts, opportunities due to market uncertainty, along with a whole host of other reasons. The market seems to have certainly weathered the storm in spite of a generally gloomy economic state.

The bridging finance sector has leapt further into the spotlight over the last few years and hopefully, with ever increasing confidence in lenders and the products they provide, bridging finance will become a mainstay in the property funding process for years to come.

To view the Bridging Trends 2022 infographic and the Q4 data, please visit www.bridgingtrends.com